Gold has a monopoly on real money

Gold has a monopoly on real money

Digital gold is as useful as digital oil or digital pork bellies

I’ve already bashed crypto once this week. But as interest rates remain depressed and people continue to desperately search for something to do with their money, I feel like bashing it again.

I’m happy to take a contrarian stance on this, in the knowledge that crypto bulls are likely to ridicule me for it. After all, I’ve known about bitcoin (BTC) and the crypto space for much longer than the average person, but I’ve not participated in the rally.

It has been difficult to watch Bitcoin rising over the years. My problem is that if I can’t understand why something is valuable, I can’t force myself to buy it.

I want to focus on the idea of bitcoin as “digital gold”.

If you read the Bitcoin white paper from 2008, you find that gold is mentioned in only one context:

The steady addition of a constant of amount of new coins is analogous to gold miners expending resources to add gold to circulation. In our case, it is CPU time and electricity that is expended.

As you can see, the author does not exactly claim that bitcoin is “digital gold”, but they do make an analogy with gold mining.

The perception of bitcoin as “digital gold” can be seen in its artistic renditions. It is usually portrayed as a gold coin:

The objection to this comparison is so obvious, that it barely needs to be said: there is no actual coin, gold or otherwise, underlying bitcoin.

In other words, bitcoin is a real coin only in the same sense that this is a real cat:

(Ironically, there has been a thriving market in crypto kitties for several years now.)

The lack of physical substance makes all comparisons to real gold illogical, in my view.

I suppose that for many people, when they think of gold, they imagine huge stacks of bullion bars in a vault at the Federal Reserve or in a Swiss bunker.

They imagine these bars sitting in the same place for many years, gathering dust.

Investors might buy and sell it, but the gold itself doesn’t know or care about that: it just sits there.

As Warren Buffett says:

Gold gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.

If gold just sits there, doing nothing, then why can’t Bitcoin be valuable too? Bitcoin is also capable of just sitting there, on a ledger, doing nothing for anybody.

The fallacy is that this ignores gold’s usefulness, even if this usefulness is delayed for a very long time (even indefinitely) by the act of investing in it.

The point is that gold can be used for almost anything. It could be argued that it is the most useful metal of them all.

Gold is suitable for monetary and investment purposes precisely because it is so useful. And its status as a medium of exchange can be traced back to its usefulness and wide popularity.

But what about the usefulness of Bitcoin, and other cryptocurrencies?

You can’t make a crown for your teeth out of Bitcoin. What can you actually do with it (apart from get rich by speculating in it)?

Again, I come back to the white paper. It is titled:

Bitcoin: A Peer-to-Peer Electronic Cash System

The first sentence is:

A purely peer-to-peer version of electronic cash would allow online payments to be sent directly from one party to another without going through a financial institution.

Bitcoin was very clearly designed to be used as a currency.

In the very early days, proponents believed that economies would voluntarily switch over to using Bitcoin, because it was a superior currency to those currently in use.

But that hasn’t happened, and many proponents have given up on that vision.

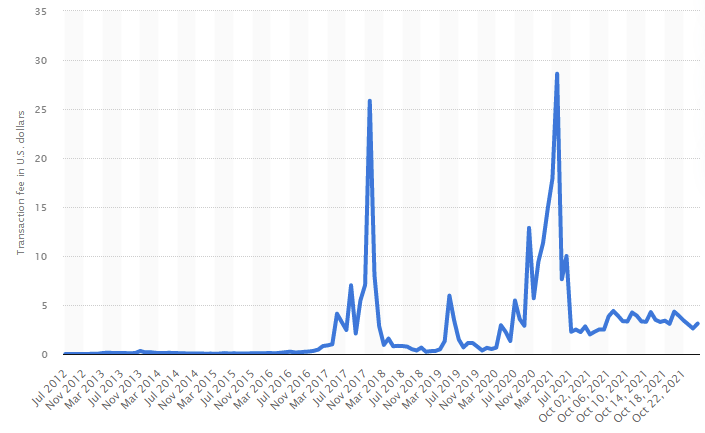

The average transaction fee for a Bitcoin deal is currently $3, and it is liable to spike when the network gets congested. Who’s going to buy a stick of chewing gum with a $3 cost on top?

There have been many efforts over the years to make bitcoin more user-friendly and affordable for small transactions, but the technology still isn’t there to make this a realistic option.

The best that Coinbase can currently offer is a 2.49% transaction fee.

The fees to use fiat currency at traditional banks can be annoying, but I’m not aware of any traditional bank that charges 2.49%, just to spend your own unborrowed money!

Therefore, since Bitcoin is not yet a useful medium of exchange, it is instead viewed as a store of value.

And the amount of value it stores has increased immensely: the Bitcoin market cap is now pushing $1.2 trillion.

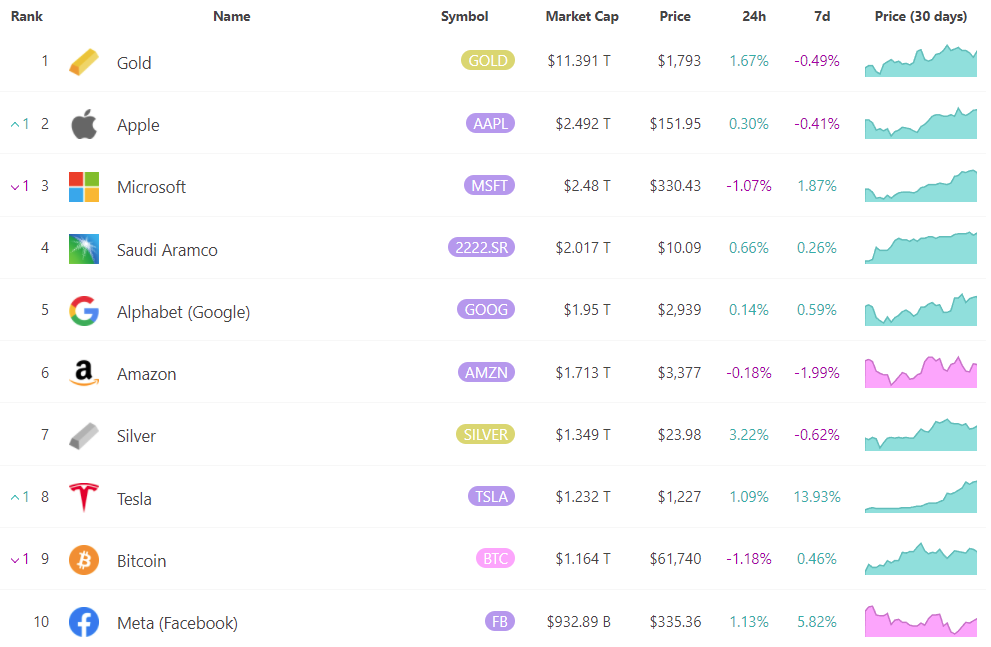

Let’s remind ourselves where that puts Bitcoin in the grand scheme of valuable assets:

As you can see, it’s up there in the list of the world’s 10 most valuable assets.

But our old friend gold remains at the top of the tree, with a market cap nearly ten times that of Bitcoin.

Many enthusiasts will see that as an opportunity for Bitcoin. After all, if gold can be worth $11 trillion, why can’t Bitcoin be worth $11 trillion?

I suppose anything is possible.

But for those of us who think that Bitcoin is less useful than tulip bulbs and that the crypto market is insane, I think we should seriously consider the possibility that crypto risks may have become in some sense “systemic”.

For example, the world’s 8th most valuable asset, Tesla (TSLA)1, has achieved that status partly as a result of taking part in the crypto bubble. Tesla accounts for 2.5% of the value of the entire S&P 500 index.

It’s not the only business with a serious amount of crypto exposure, whether that is direct balance sheet exposure or indirect sentiment exposure.

The popular trading platform Coinbase (COIN), mentioned earlier, has a market cap of $72 billion, which is ten times its predicted revenues. A crypto crash would be disastrous for this stock.

More generally, if the crypto train stops, it will leave plenty of leveraged investors looking for ways to fill the gaps in their portfolios.

During the collapse of 2009, I remember speaking to a trader who had done very badly in UK stocks. He was obviously quite sore about it, but he still maintained that his stock picks had been excellent.

The companies he had picked didn’t have any problems, he insisted, but the banking collapse had forced other traders to cover their losses - by selling their positions in the good companies he owned.

We will all have our excuses. But if the current mania ends badly, I don’t think anybody will be able to argue that they thought crypto was a safe investment.

The truth is that nearly everybody will have seen it coming, or known that it was possible - but hoped they would be able to get out before the music stopped.

Regards

Graham

Disclosure: the author has a long position in gold contracts and short positions in Tesla (TSLA).

Very good said!Bitcoin and Co are trade sardines.