IG Group powers ahead

IG Group powers ahead

I might soon forgive them for spending $1 billion on a company with a silly name.

This morning saw full-year results from IG Group (IGG), the #1 CFD company in the world and the biggest spread betting provider in the UK.

This share is an important part of my personal portfolio:

While it has enjoyed leading market share in the UK for decades, its efforts in the United States have always been inconsequential.

But that all changed with its $1 billion purchase of US retail brokerage tastytrade last year.

This is a brash, fun platform for futures and options trading. It acts like a news channel with a brokerage attached:

Tastytrade has nearly 300,000 subscribers on its YouTube channel - though its recent videos don’t get more than 10,000 views.

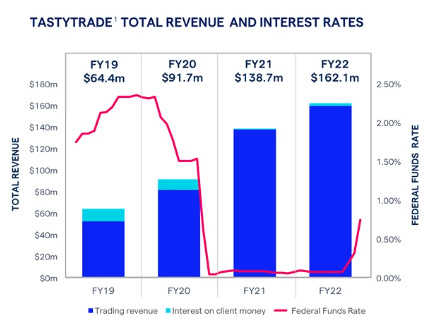

Maybe that doesn’t matter, because revenues in its first year with IG are up by one-sixth. Its trajectory over the past three years is excellent:

But IG still has a lot to do, to justify the $1 billion price tag for this deal.

The message from IG is that we need to consider the enormous addressable market of American traders that IG can now access, through tastytrade. We shall see!

It is true that without this acquisition, IG’s revenues would have been flat in FY 2022. Instead, we get a 14% increase in the top line.

Declining margins

Unfortunately, it was an expensive year for IG. Tastytrade is expensive to run, and there were many one-off costs, too.

In total, operating costs rose by a massive 28%. This slowed the growth of profitability, and caused the pre-tax profit margin to fall below 50% (still a very respectable figure by most companies’ standards!).

The profit margin is anticipated to fall further in the current year, before returning to the high-40s over the medium-term.

Fat margins are one of the features of IG that has kept me in the stock over the years.

While I’d love if they could keep this metric over 50%, I’m willing to accept a lower number if we see good continued top-line growth.

You don’t trade here any more

Covid caused a retail trading boom, as bored people stuck at home opened new spread betting accounts.

Many of these rookie traders have now reduced their activity. Active spread betting/CFD clients are down 8%:

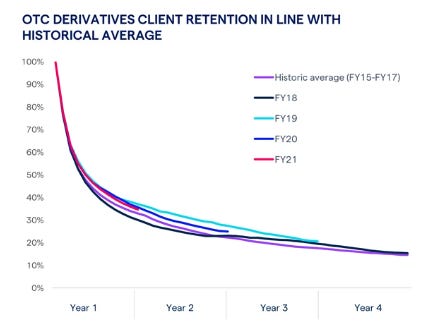

At the same time, CEO June Felix has produced evidence that the cohort of traders who signed up in FY 21 (the red line) are behaving similarly to prior cohorts.

The question is: will these rookie traders want to trade as heavily in future years as the previous cohorts did?

I also note there was just 4% client growth in IG’s stockbroking business. IG’s product is superior to many of the traditional UK brokers, so I’m not sure why they aren’t growing faster.

Share Count: Ups and Downs

The acquisition of tastytrade resulted in the issuance of 61 million new IG shares.

This has hurt IG’s earning per share, which is down by 7% to 92.9p.

Normally, I hate to see a rising share count at my companies. When the share count has risen because of acquisitions I’m iffy about, that’s doubly bad.

But IG has rescued the situation for me, by announcing a £150m share buyback.

IG is a wonderfully cash-generative business, receiving cash instantly whenever its customers trade.

Because of continued excellent cash generation, it finished FY May 2022 with “own funds” (i.e. net cash) of £1.25 billion. The balance sheet also had tangible value of over £1 billion.

It covered its regulatory capital requirement twice over.

Since it has far more cash than it needs, and its shares are on a trailing P/E multiple of just 8.4x, I’m delighted to see it announce this buyback.

If the buyback was carried out at an average price of £8/share, it would reduce the share count by c. 19 million. This would erase almost a third of the dilution caused by the tastytrade acquisition.

In time, I would like to see all of the tastytrade dilution wiped out. But this is a good start.

What do you think - would you invest in IG Group at its current valuation?

I’d really appreciate if you could again hit the “heart” button, to let me know you enjoyed this article. Thank you!

Best regards,

Graham

PS: You may have noticed that I published a new article on the performance of my personal investment portfolio yesterday. It’s available for paid subscribers - see here.

Not familiar with the name in detail. But surely spreadbetting/CFD where IG lead are small markets in the US due to lack of CGT benefits over there? Hence I'm not sure why you would acquire a subscale US broker, that can't compete on cost with Interactive (etc.) and saw a massive benefit from COVID. Or am I missing something?

Slightly quixotic to issue 61m new shares then immediately do a share buyback …