The blockbuster spin-off of 2022 is here

The blockbuster spin-off of 2022 is here

Get used to the name. You'll be hearing a lot more about this one.

When I hear the word “spin-off”, I sit up and take notice.

Ever since reading Joel Greenblatt’s poorly-titled masterpiece, You Can Be a Stock Market Genius, I’ve known that there are structural reasons for spin-offs to do well.

Because when owners of a large company are given shares in a smaller spin-off, they often have no interest in it!

The spin-off might be too small, or too complicated, or in the wrong sector.

So what happens? Well, the owners of the parent become natural sellers of the stock they’ve been gifted.

And while the price of the spin-off is depressed by all this selling, the spin-off business is not sitting still.

It suddenly has the autonomy to decide its own future - its own independent Board of Directors, its own CEO whose chain of accountability has been simplified, and employees whose stock compensation is now directly tied to the success of their own business.

The outperformance of spin-offs was a feature of the stock market for decades, but it has not held true in recent years. For example, the S&P has outperformed Invesco’s S&P Spin-off ETF since 2019, by a wide margin:

Does this mean the party is over? I doubt it.

Remember that small-cap stocks have underperformed in recent years. That alone could be a significant factor.

My guess is that institutional investors are about as sophisticated as they have always been, and will continue to sell spin-off shares more aggressively than they should.

All of which brings me to Haleon (HLN), a company that traded on the London Stock Exchange for the very first time yesterday.

At the latest share price of 303.5p, the company is capitalised at £28 billion. This puts it just inside the top 20 largest companies in the FTSE-100.

What is it?

Haleon is (or was) the consumer division of pharmaceutical giant GSK (GSK 0.00%↑), jointly owned with Pfizer ( PFE 0.00%↑ ).

As explained in an investor update back in June 2021, GSK felt that a spin-off would “unlock the value” of this division.

Meanwhile, the rest of GSK would be able to focus on fighting disease through vaccines and specialty medicines.

Haleon’s product portfolio includes some names you’ll recognise, no matter where you live:

As this publication is called “Monopoly Investor”, and my main focus is on finding market leaders, here is some information concerning the power of Haleon’s brands:

The Group’s portfolio includes nine large-scale multinational Power Brands… which represented 58 per cent. of revenue in FY 2021.

Of these nine brands, Voltaren, Advil, Otrivin, Sensodyne, Polident and Centrum are the number one or number two brand in their respective sub-categories globally.

In addition, Panadol is the leading Systemic Pain Relief brand outside of the USA.

On top of these global brands, Haleon has others that are popular in particular regions:

#2 systemic pain relief brand in China

#1 heartburn brand in the USA

#1 pain relief brand in South Africa

#1 manual toothbrush brand in Germany

#1 Digestive Health brand in Brazil

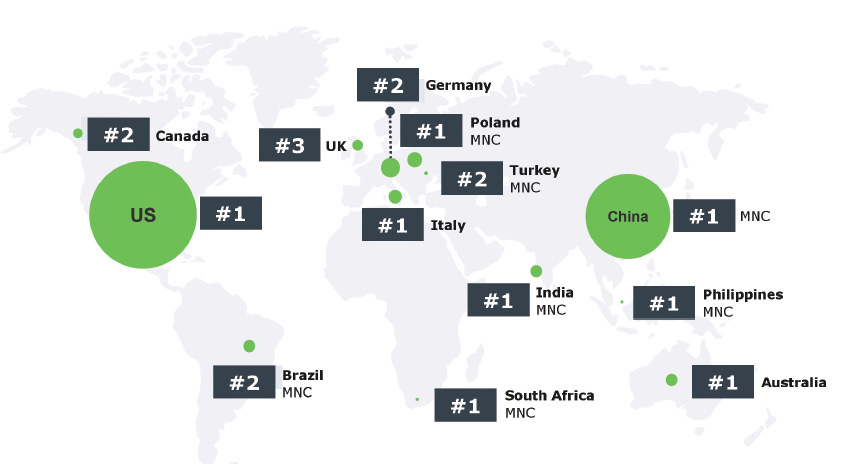

I don’t know about you, but I take a lot of comfort from seeing the #1 and #2 leadership position in so many categories. This chart shows Haleon’s combined market ranking in over-the-counter medicines and supplements around the world:

Profitability: quite good

In 2021, Haleon earned an operating profit of £1.6 billion on sales of £9.5 billion (operating margin 17.2%).

The performance in Q1 2022 looks promising: the operating margin improved, and there was an improvement in sales and profits over Q1 2021.

As for the balance sheet, the pro forma numbers show that Haleon is carrying net debt of £10.3 billion.

That might sound high, but Haleon still expects to get an investment-grade credit rating.

So, is it worth a second look?

My answer to this question is: yes, definitely!

For one thing, Pfizer signalled its intention to sell its massive 32% stake. This could very easily depress the share price, creating an undervaluation.

Valuation - at its current share price, the enterprise value of Haleon is £38 billion.

This gives a trailing EV/EBIT multiple of around 23x. Not cheap by any means, but there is scope for it to get cheaper when Pfizer starts selling.

Another point is that Unilever (LON:ULVR) (UL 0.00%↑) offered £50 billion to buy it, earlier this year.

If it was worth that much to Unilever, maybe it is worth at least £38 billion to you and me?

Let me know what you think in the comments!

Best wishes,

Graham

PS: I’d really appreciate if you could again hit the “heart” button, to let me know you enjoyed this article. Thank you!

Thanks Graham. Reminds me of the Indivior split. It stumbled around for a while, but then really found its feet. Will keep an eye on here. Already hold a tiny cache.

Thanks Graham Looks interesting - will do a bit more research andwatch for Pfizerrs sales