Mickey Mouse bounces back

Mickey Mouse bounces back

Was it ever in doubt?

Last night, Disney released results for the quarter ending January 1st 2022 (which I will refer to as Q4 2021*).

The Walt Disney Company ($DIS)

Share price: $156.

Market cap: $284 billion.

This is a stock I analysed for subscribers last summer.

I talked about Disney+ being “Netflix for Kids”, and noted the already significant recovery towards pre-Covid levels of revenue and profitability.

The recovery continues in earnest:

Total quarterly revenues are up by 34% compared to last year and are now above the equivalent pre-Covid quarters.

Let’s consider the company’s two major segments:

Parks, Experiences and Products almost returned to their pre-Covid revenues ($7.2 billion versus $7.6 billion in Q4 2019).

Disney Media and Entertainment Distribution (including Disney+) achieved new record revenues for the quarter of $14.6 billion (vs. $12.7 billion in Q4 2020, and $13.3 billion in Q4 2019).

We can’t eat revenues, of course. Operating profits were as follows:

Parks, Experiences and Products were back at pre-Covid levels, at least nominally (there has been quite a lot of inflation over the last two years, after all!)

If you’re happy to round to one decimal place, then operating profits in this segment were the same as the most recent pre-Covid quarter ($2.5 billion).

Profits at Disney Media and Entertainment Distribution are down compared to prior years ($800 million vs. c. $1.5 billion in prior years).

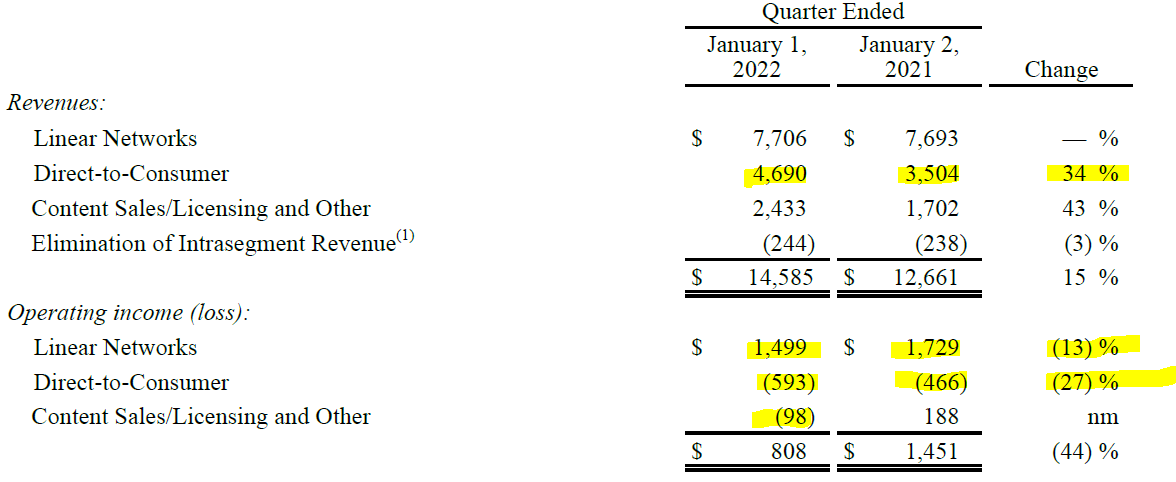

Let’s get the breakdown of this important segment, which includes the company’s TV channels and Disney+:

“Linear Networks” (TV channels) had a very mixed performance with the reduced operating income being blamed on higher programming and production costs, increased marketing spending, and lower political advertising revenue (Biden’s election victory was in the comparative quarter).

I’m not sure what we can take away from this except perhaps that TV broadcasting is not immune to the inflationary pressures faced by the rest of the global economy, although there were also several Disney-specific reasons for the increased costs this quarter.

“Direct-to-Consumer” saw the combination of high revenue growth with significant growth in losses that we expect from a company in startup mode.

Disney+ saw subscribers grow by 37% to 130 million (compared to the same quarter last year). Most investors will have no problem at all with some losses being incurred while this growth opportunity is embraced and maximised.

Just like Netflix, Disney is raising prices and its average monthly revenue per Disney+ subscriber increased from $4.03 to $4.41.

I have to believe that there is plenty of scope for this to grow in the future.

I also note that the 130 million-strong subscriber base is 59% of the size of Netflix. For a service that only launched in November 2019, this is nothing short of extraordinary! (Netflix launched in 2007).

Disney also has a combined 66 million subscribers at ESPN+ (which grew by 80% last year) and Hulu. So the entire number of paid streaming customers at Disney is 196 million, i.e. nearly 90% of the size of Netflix.

Content Sales/Licensing results suffered from losses on titles released in cinemas during the quarter. This is a serious point of concern - is the cinema sector doomed to be much smaller than it was pre-Covid, now that streaming is ubiquitous and that so many titles are being released directly to streaming services?

Under this interpretation, the progressive in the Direct-to-Consumer segment is less impressive and becomes more of a replacement for cinema revenues than a stand-alone growth opportunity.

Key takeaways

The fundamental thesis I described in my previous article is intact.

The synergies at Disney are intact and are very easy to understand, as the audience returns to theme parks in huge numbers and sales of Disney-branded products remain strong despite the impact of some Covid-related retail closures.

The addition of a D2C streaming service in the form of Disney Plus, where new titles can be released without the need for any intermediary, is an enormous opportunity and it’s understandable that Disney would choose to invest heavily in it at this early stage.

Valuation is difficult, for a few reasons:

how to estimate the size of the opportunity of Disney+? Can it achieve bigger size than Netflix? at what pricing point per month?

if Disney+ succeeds at massive scale, does it mean that cinemas are more or less obsolete?

similarly, will the relevance of Disney’s traditional TV networks decline as streaming takes a bigger slice of the TV pie?

My preferred valuation metric for Disney is EBIT/EV, calculated as a yield. I estimate this as 4.2% for 2022, rising to 4.9% by 2024 if forecasts are hit.

That’s not cheap by any means. But for a company this special, it just might be worth it.

Best regards,

Graham

*I will refer to this quarter as Q4 2021 even though the company refers to it as Q1 2022, and will treat all other quarters in a similar fashion.