What if Netflix was just another TV channel?

What if Netflix was just another TV channel?

Paying five times sales wouldn't make much sense.

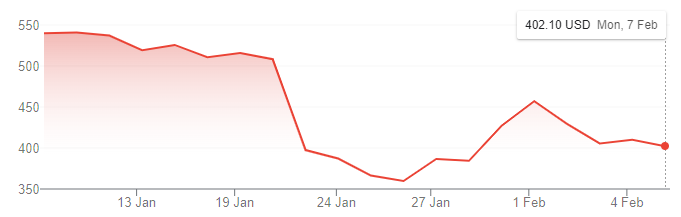

Netflix (NFLX) has been in the headlines recently, after a serious fall in valuation:

The market cap is now standing at $178 billion, down from over $300 billion at its peak in November.

I wrote about the stock back then, and tried to be as fair as possible.

On the one hand, I applauded the company’s successes, and said that it did have the potential to grow into its valuation.

But I also said that I would prefer to own stock in some of its competitors, namely:

YouTube ($GOOGL, which I do own).

Twitch and Amazon Prime ($AMZN)

Disney Plus ($DIS)

These competitors have synergies and competitive advantages which I feel that Netflix lacks (YouTube and Twitch, for example, don’t have to buy any content!).

I also noted that broadcast and cable networks still controlled significant market share of US TV time. The streaming market will inevitably keep growing, but so will the investment dollars flowing into it.

The key question is: why will Netflix be able to earn higher returns than its competitors, and will those returns be attractive at the scale implied by its market cap?

A serious slowdown

Netflix added 8.22 million net new subscribers in Q4 2021, which was only 3% lower than the forecast number.

Worse was the forecast for Q1 2022, which is predicted to yield 2.5 million new subscribers.

The corresponding figure for Q1 2021 was 3.98 million.

This slowdown has brought bearish arguments back to the forefront of investors’ minds. In the face of competition from extremely well-funded competitors, and in the absence of stellar growth, it’s easy to become spooked.

Year-on-year revenue growth of 18% in 2021 is perfectly fine in most circumstances, but not when your stock is trading at five times sales. Indeed, this is the slowest annual revenue growth by the company since 2012 - and the situation was very different back then!

A broken business model?

The question mark in this subheading is important. I don’t want to unfairly jump on a bearish bandwagon for a company which was, is and will probably continue to be highly successful in many respects.

However, it does appear that the market and the wider public has begun to focus more of its concerns and attention on the issues I raised in last November’s article.

For example, last week Variety Magazine published the following headline:

YouTube Ad Sales Hit $8.6 Billion in Q4, up 25% and Topping Netflix Revenue for Quarter

YouTube Ads are only one of the ways that the platform is monetised.

And did I mention that YouTube doesn’t have to pay for any content?

Which would you prefer to own: a media company which attempts to sell content for more than the cost of creating or buying it, or a larger media company which doesn’t have to take any content-related risk at all, because its users will happily upload content for free?

That is the essence of the difference between Netflix and YouTube.

Netflix is the gambler in the casino, buying lots of content (making lots of bets) and hoping that a few of them pay off. Sometimes, it wins big, but it can never be sure when that is going to happen.

YouTube, on the other hand, is the casino itself. Its customers have to produce the content (make bets), and YouTube simply takes a guaranteed percentage of the action. Twitch (owned by Amazon) operates in a similar fashion.

If I stretch this analogy further, where does it put the likes of Apple TV, Amazon Prime and Disney Plus?

Let’s say they are the VIP businessmen in the casino. The high rollers, if you will.

They’ve already made plenty of money from doing something else (selling phones or books, for example), and so they are far more relaxed about whether or not they make money at the casino. They can afford to keep betting, no matter what.

It’s an increasingly uncomfortable situation for Netflix. On the one hand, there are the “platform” competitors which take no content risk at all, are extremely diversified with many thousands of content creators, and have algorithmic systems which constantly serve up the most interesting and entertaining content to the right users.

And on the other hand, you have the extremely wealthy technology and media giants who have set up streaming services almost as an afterthought: Apple TV, Amazon Prime and Disney+.

If Netflix isn’t as rich as these companies, and can’t create synergies with any other products in the same way that these companies can, then is there any reason why Netflix should succeed instead of them? I’m struggling to think of one.

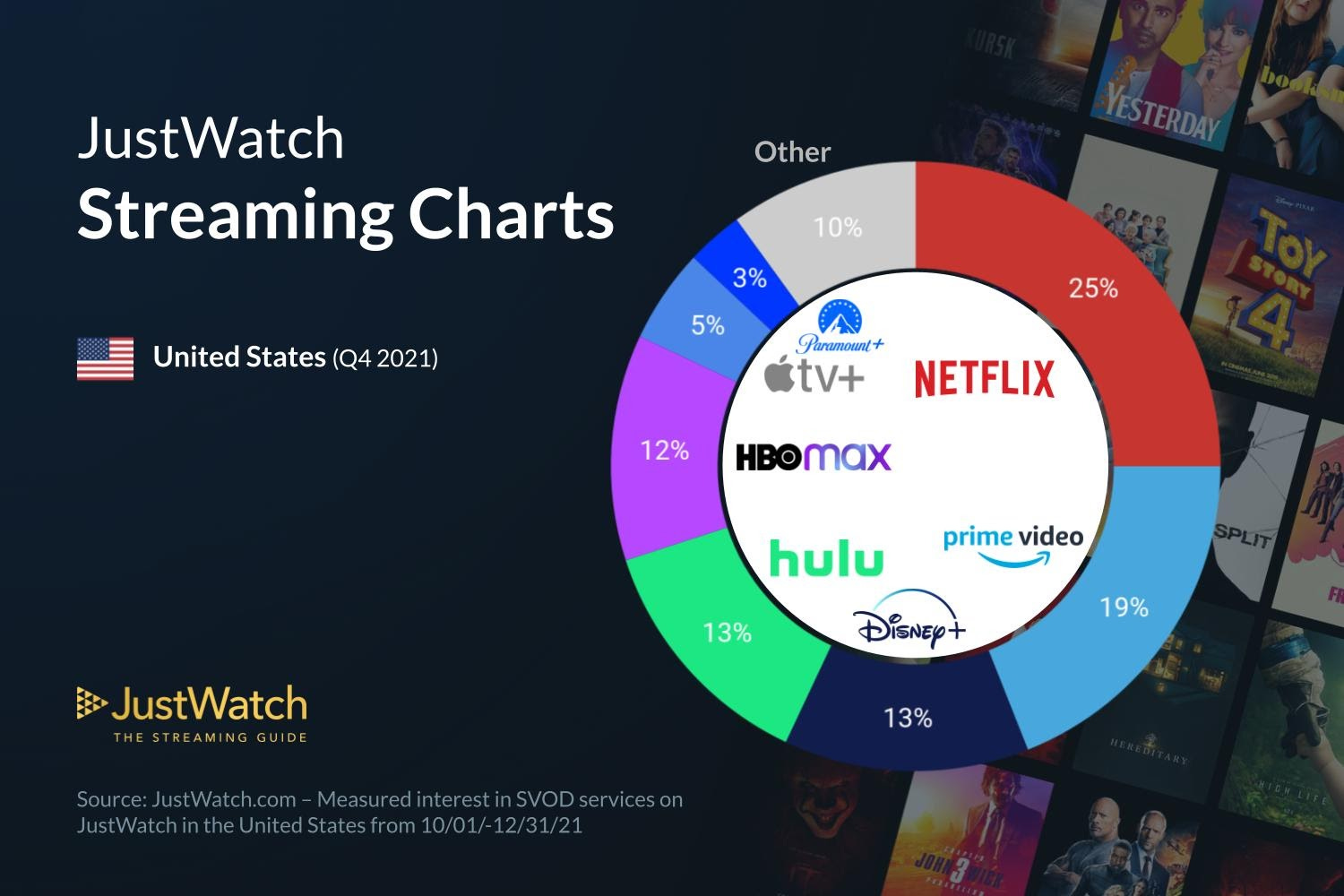

This helpful chart from JustWatch (source) lays out the recent competitive landscape. Don’t forget the importance of Hulu (owned by Disney) and HBO Max (ultimately owned by AT&T):

The outcome: last mover advantage and increasing fragmentation

Speaking very broadly, this is what I expect will happen over the next five years:

The streaming market will continue to grow. This, combined with the Netflix first-mover advantage should enable continued impressive top-line growth (market forecasts suggest that revenue will increase from $29.7 billion in 2021 to $42 billion in 2024).

However, one or more of the media/tech giants will generate major synergies between streaming and its other product lines. Having learned from the experience of Netflix, and with the help of these synergies, it will enjoy a “last-mover advantage” and a significant competitive superiority. This will cause Netflix to lose its market share lead both in the US and globally.

At the same time, due to the absence of significant barriers to entry, continued fragmentation may occur such that increasingly specialised streaming services become viable. In the same way that Disney Plus is geared towards families, new services in the future might be more targeted to particular demographics. This will be good for consumers but it will work against the generation of large monopolistic profits by a generalist such as Netflix.

Conclusions

I’m not ready to suggest that the demise of Netflix is imminent, and that it already resembles a video rental shop in its usefulness and future profitability.

When the market cap was at $300 billion, I thought it was possible that it could grow into that valuation on a long timeframe.

With the market cap now “only” around $180 billion, growing into its valuation has become all that much easier (if forecasts are hit, the 2024 P/E is “only” 21x - bargain!).

My worry is that I just don’t see a comfortable endgame for the company. As time passes, it might end up being viewed as just another streaming TV service in a long list of high-quality streaming TV services.

Indeed, perceptions and reality are already going that way.

Let me know what you think!

Another interesting article. I agree with this analysis. Simply put, Netflix don't have an easily defensible moat although the brand is exceptionally strong. It's a zero sum game between the streaming platforms and competition is going to be fierce. I expect to see some consolidation in this sector because consumers will get subscription fatigue if they have to subscribe to so many fragmented services in order to get the content they crave. Perhaps a massive takeover deal of Netflix could be in the future? Might it be a juicy target for Disney, Amazon or Apple or maybe even one for FB / Meta since they don't really have skin in this game at present.

Interesting take on Netflix. I hold a small amount in my son's JISA. The selloff has caused a 0.9189% loss to the JISA so not at all catastrophic. (37% of the JISA is in BRK.B)

I would love to see a bear/bull debate between you and Sean Stannard-Stockton at Ensemble Capital https://intrinsicinvesting.com/2022/01/24/netflixs-man-overboard-moment/!!

I am sure you have read their blogs on Netflix.

Cannot say I completely disagree with you but I think they have a lot of room to increase subscription price without losing subscribers. As to content, they only have to get it right once every so often to keep people subscribing.

While I believe you are right that I would rather have Google/YouTube's business model (why oh why did I not invest a couple of years ago when I thought they were too expensive) I don't think they are directly comparable. You don't have to subscribe to YouTube and the content is, IMO, very different.

I think it is not unreasonable to see the subscription to Netflix increase by say 10 bucks over say three to five years. That is an additional $26,640,000,000 a year in revenue (that is roughly double current revenue) and that is without subscriber growth. And looking at subscriber numbers (especially penetration) at www.comparitech.com/tv-streaming/netflix-subscribers/ I would say they still have room outside of the US and some small countries for subscriber growth.

Anyway, it will be interesting to see how this plays out.

Regards

Michael